Have you seen the 52 week Savings Challenge? Well it has really gone viral and is a very easy way to beef up your savings account with at least $1300.

Best of all this is a fairly painless process that everyone can do! If you are a person that is living paycheck to paycheck and just can’t seem to get going on an emergency fund, I can’t recommend this strongly enough.

Even if you can’t get through the entire year and you just do this for halfway, you will still be adding $700 to your savings account which is a major WIN!

I know some of you might be pretty on track with your savings goals so this might be used in a different way for you. Perhaps you can get the children started with this process and they can see a savings account really grow over time!

Or guess what? $1300 is roughly a mortgage payment for many of us. And did you know making ONE extra mortgage payment per year can cut a whopping FOUR years off a 30 year mortgage? Even better- on a $200,000 mortgage that will save you a gigantic $32,000 in interest over the life of the loan. Crazy!

Another idea would be to use this savings account for a specific goal- maybe a pricey item you have your eye on, a little vacation or use this process to save up for next Christmas and the savings you generate can take care of all your holiday expenses!

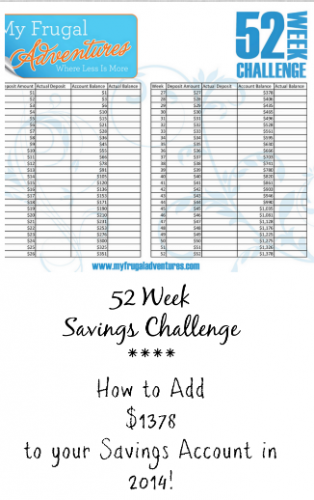

There are a few ways to go about this process. The first is to start with the chart that I have attached below. The idea is to use a 52 calendar week year and save the same amount of money as the week.

So for the first week of January, you would have put $1.00 in your savings account because that is week #1. For the second week of January you would save $2.00 because that is week #2. Each week the amount you deposit into savings is going to go up by $1 until your last deposit is $52 for the final week (week #52). If you do this diligently, you will have saved $1,378 by the end of the year!

The nice thing is that for the first several weeks you probably won’t even notice the amount you are putting aside. I am posting this a little later then I had hoped so you have to catch up a bit. (Sorry!)

If you do the original chart starting with $1.00- here is how much you need to get started today:

- Week 1 $1.00

- Week 2 $2.00

- Week 3 $3.00

- Week 4 $4.00

- Total $10

For many of you getting the $10 together won’t be a big deal but for others it can feel overwhelming to squeak out a little extra in the budget each week. (Totally get that- been there done that!)

But can you take lunch just one day this week instead of buying out? Skip one fast food run or 2 Starbucks trips? Extend that haircut just one extra week? Make it a game and get the kiddos to help you search through the house and cars for any loose change? (Crazy how that change can add up!)

Here is my favorite simple way to save– on every Target trip my 8 year sits in the cart and as I add items she scans them with the Cartwheel app looking for coupons. That is something I don’t always make time to do but it keeps her busy and we always save a few extra dollars at checkout.

And now sock it away in a jar and get ready to pony up the $5 for next week! Before you know it your dollars will turn into hundreds and the hundreds will be over $1,300. A huge blessing to anyone’s savings account.

And here are some ideas to modify this plan to better suit your household:

Many people like to work backwards. This is helpful for 2 reasons- #1 you aren’t putting the largest amount in savings during the month of December. Perhaps you find it easier to tighten the belt in January and start backwards and then have your smallest savings month during the holidays. You will also earn more interest by working this program backwards so bonus!

If you want to work the plan backwards, you need to find $202 to catch up. That is a little more challenging so here are some ideas– anything at all you can put up on Craigslist or Ebay? What about Gift cards you may have received? Dig them up and see what the balances are- you can sell them on Ebay or Raise.com for cash. Any items you got for Christmas you don’t nee or want and you can return? Cash in on old electronics- Amazon has a great trade in program. Cut coupons!! Be diligent this month about coupon clipping and see if you can squeak the money out of your grocery bill. Quit eating out for this month. Period. Painful yes but it adds up crazy fast! When my husband and I were paying off our debts we literally spent about $60 for that entire year on “dining out”. That included coffee with friends, quick lunches, takeout dinner, restaurants all of it. Yup $60 for.the.entire.year.

If this program looks doable for you, why not double the savings? You would have almost $2,800 by the end of the year!

Maybe you can double it or maybe you can enlist the children to see if they can get involved in adding to the savings pot- this is especially great if you have a goal for the money (like a vacation). Or maybe you and your spouse have a little competition on this one and keep track of what each of you can add to the jar each week.

So hopefully some of you might give this a shot. I would suggest printing this out- that is what worked for us. I loved having the constant visual reminder of paying off our debts and then the visual of seeing the progress as we started an emergency fund. It made it a lot easier to say no to that pedicure when I saw the progress I was making toward our goals.

Should you find a week where you have a little extra money maybe you can jump ahead. For example we had pizza last night to the tune of $22. If I was on this savings challenge and decided to skip pizza and make dinner at home, I could redirect that $22 into my savings jar and mark off week #22.

If you are already on this challenge or if you did this last year, I’d love to hear your tips and ideas!

Download the free printable 52 Week Challenge Worksheet Here.

Wow! Thanks for posting this! I love this idea! Thank you!

I think it’s easier to save $4-5 a day, everyday and end up with more or less the same amount of savings at the end of the year. This is a good savings game though.